Friend of Fringe Finance Mark B. Spiegel of Stanphyl Capital released his most recent investor letter last week, with his updated take on the market’s valuation and Tesla.

Mark is a recurring guest on my podcast (and will be coming back on again soon hopefully) and definitely one of Wall Street’s iconoclasts. I read every letter he publishes and only recently thought it would be a great idea to share them with my readers.

Like many of my friends/guests, he’s the type of voice that gets little coverage in the mainstream media, which, in my opinion, makes him someone worth listening to twice as closely.

Mark was kind enough to allow me to share his thoughts from his December 2022 investor letter, where he noted that his fund was up 17.4% for the month, rounding out a year where he finished up 75.5% net of fees.

In his most recent letter he opens up about a new short position, his thoughts on Tesla, how he’s positioned overall in the market and other names he owns. He also, in my opinion, absolutely nails the current (bear) case for the overall market heading into 2023.

Mark On Macro And Tesla

December 30, 2022

Before I continue, I want to clearly state that the chance of this fund’s 2023 performance being anywhere near that of 2022’s is roughly equal to the chance of Elon Musk offering me a board seat at Tesla. (For the record, I would not accept such an offer as I don’t want to go to jail!) Okay, now that that’s out of the way…

Tesla’s inevitable meltdown (alright, so I was a mere eight years too early!) was a big contributor to this year’s performance (and we remain short it, as I believe it has another 90% to go), as were our other short positions in the S&P 500 (via SPY) and, early in the year, the garbage-stock ETF ARKK (which I covered way too early, leaving lots of additional profit on the table).

Another meaningful December contributor was an arb position we’ve had on for several months but I haven’t written about here as it was crowded: short AMC shares and long an equal number of APE shares—two essentially identical securities from the insolvent AMC movie theater chain that—thanks to the deliberate ignorance of AMC’s “meme stock” shareholder base—had a massive price disparity between them. In December the inevitable happened when the company announced a financing deal that will merge the two share classes and end that spread; their prices subsequently converged significantly and I anticipate further convergence in January.

Meanwhile, we continue to carry a large SPY short position, as I believe the major indexes—although not all individual stocks—have considerably more downside to go, the inevitable hangover from the biggest asset bubble in U.S. history. Stated simply, there’s no way an “everything bubble” built on 0% interest rates and $120 billion/month in quantitative easing can not implode when confronted with near-5% rates and $90 billion a month in quantitative tightening.

Although the current rate of 6% to 7% year-over-year inflation (down from over 8%) is unsustainable, I believe we’re in for a new “inflation floor” of around 4% (double the Fed’s already-too-high 2% target) thanks, in the near-term, to a new tailwind in commodity prices as China ends its “zero-Covid policy” and bails out its real estate industry while Biden ends his SPR drawdown and continues his war on fossil fuels.

Longer term contributors to that higher inflation floor will be expensive “onshoring,” wage increases due to fewer available workers, and perpetual government budget deficits (most recently exemplified by the egregious new “Omnibus Spending Bill”). And even if there’s a temporary dip in inflation (as we appear to be seeing now), the Fed does not want to reverse rates too soon and repeat the 1970s:

Even an early-2023 Fed interest rate “pause” at 4.75% (and remember, a “pause” is not a “pivot”!) would, combined with $90 billion a month in ongoing QT, make current stock market valuations unsustainable, as stocks are still expensive.

According to Standard & Poor’s, with 99% of companies having reported, Q3 S&P 500 GAAP earnings came in at around $44.41, which annualizes to $177.64. (And these were the sixth highest quarterly earnings in history; i.e., they were not “trough.”) A 16x multiple on that—generous for a rising rate, recessionary (or even just slow-growth) environment—would bring the S&P 500 down to 2842 vs. its current 3839. And remember, just as in bull markets PE multiples usually overshoot to the upside, in bear markets they often overshoot to the downside. A bottom formed at a considerably lower multiple is not unfathomable.

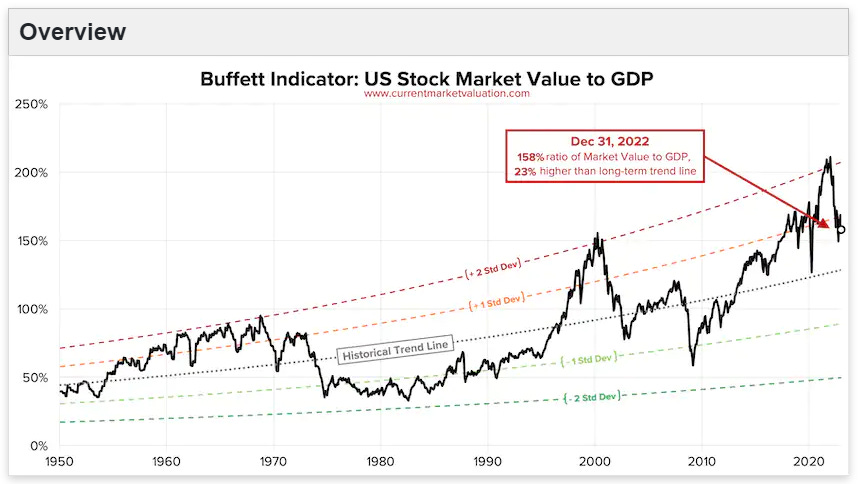

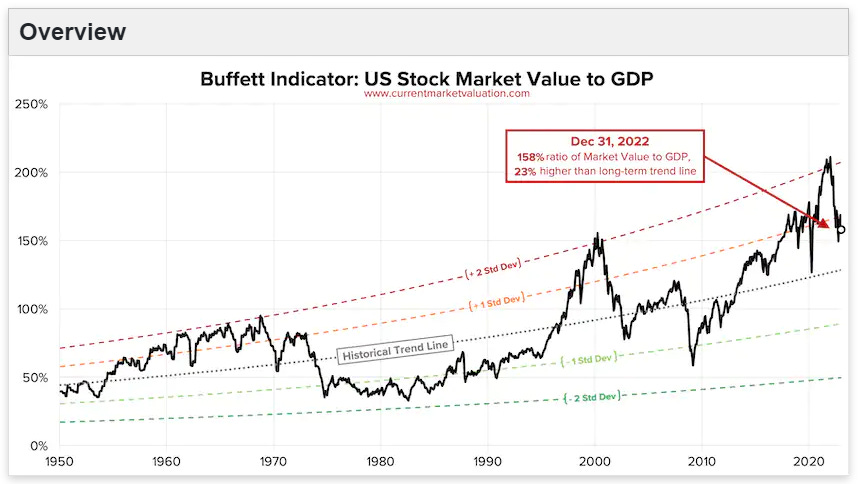

Additionally, we can see from CurrentMarketValuation.com that the U.S. stock market’s valuation as a percentage of GDP (the so-called “Buffett Indicator”) is still very high, and thus valuations have a long way to go before reaching “normalcy”:

For some historical perspective on current market excitement about inflation reports that are trending lower, keep in mind that when the 2000 bubble burst and the Nasdaq was down 83% through its 2002 low and the S&P 500 was down 50%, the rates of CPI inflation were just 3.4% in 2000, 2.8% in 2001 and 1.6% in 2002.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}